North Macedonia is negotiating a strategic project to build two hydropower plants, Čebren and Galište, in an investment estimated at EUR 1.2 to 1.3 billion, according to Prime Minister Hristijan Mickoski. A tender for building the Čebren pumped storage hydropower plant was annulled by the previous government in early 2024.

The country intends to finance the construction of the two hydropower plants with a loan from the United Kingdom, the prime minister said. He indicated that funding has been secured for several government projects, partly through loans and partly through private investments, according to a statement by the Government of North Macedonia.

The Čebren and Galište project could be financed from a British loan

In the previous tender, the Čebren hydroelectric project was planned to have a capacity of 333 MW, with an option for another unit and 458 MW in total.

In early 2024, the former government annulled the tender, in which Greece-based Public Power Corp. (PPC) and Archirodon were selected for the Čebren project. The authorities said at the time that they would analyze whether it would be more profitable to build Čebren with the state’s own funds or with the help of strategic investors.

A few months ago, Minister of Energy, Mining and Minerals Sanja Božinovska said projects were under development for battery energy storage systems (BESS) and pumped storage hydropower plants.

The project will last several decades, Mickoski says

Addressing the parliament today, Mickoski described the project as strategic, adding that it would not be completed during this government’s term of office. “This is a project that will last several decades,” he said. The funding will be provided through low-interest loans as a state investment, and the rest under market terms and through direct private investment, according to Mickoski.

The prime minister is also confident that the two proposed reservoirs could provide additional water for irrigation amid future climate change impacts and help boost tourism development in the area.

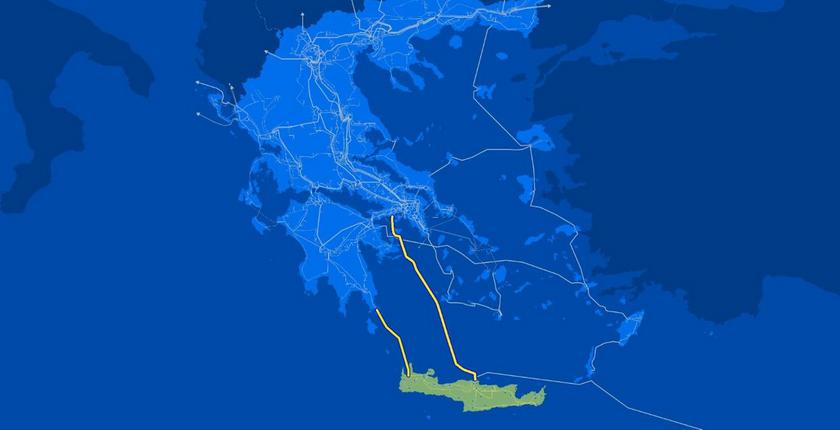

The Attica-Crete subsea power interconnector has been put into trial operation, marking a milestone for Greece’s transmission system. The country now has a high-voltage direct current (HVDC) interconnection, and its largest island is fully integrated into the national electricity system, according to an announcement by the Independent Power Transmission Operator (IPTO or Admie).

The Ariadne subsea power interconnector entered into operation on May 24 with the successful transfer of direct current electricity, said IPTO, whose subsidiary Ariadne implemented the project. The trial operation phase is expected to last throughout the summer, IPTO added.

The two submarine power links have ended Crete’s electrical isolation

Combined with the existing interconnection via the Peloponnese peninsula, the new cable has completely ended Crete’s electrical isolation, making it an energy hub with significant environmental and economic benefits for the country and the local community, according to IPTO.

The first power link between Crete and the mainland is the 174-kilometer alternating current (AC) cable linking the island with the Peloponnese. It was completed in 2021, following an investment of EUR 380 million.

The EUR 1.1 billion Ariadne interconnector is among the deepest in the world

The Ariadne interconnector, which cost over EUR 1.1 billion to build, is one of the deepest subsea power cables in the world. It consists of two 500 kV cables of 500 MW each, laid at depths of up to 1,200 meters. The construction lasted 4.5 years.

Greek Minister of Environment and Energy Stavros Papastavrou stated that the new power link has made Crete a “central pillar in the country’s energy transition,” and IPTO CEO Manos Manousakis claimed it is opening “a new chapter for the island’s energy security.”

The project was co-financed through the National Strategic Reference Framework (NSRF 2014-2020 and NSRF 2021-2027), via the European Union, with up to EUR 535.5 million.

IPTO recalled that the project consisted of many large subprojects, with contractors including Siemens, Terna, Nexans, Prysmian, NKT, and Hellenic Cables.

Energy transition in Southeastern Europe is accelerating, and the progress depends on individual countries’ strategies and legal frameworks. At the Belgrade Energy Forum (BEF 2025), representatives of state-owned power utilities and private producers discussed the different approaches to decarbonization. The domination of investments in renewable energy is unquestionable, but there are also ambitions to develop nuclear capacities, spearheaded by Slovenia. The country is already operating one nuclear reactor and is developing a project for another one.

The electricity sector in Southeast Europe still depends for a large part on thermal power plants that burn fossil fuels. In 2023, they accounted for 43% of overall output, of which two-thirds were from lignite and the rest from gas. There is a need for accelerated decarbonization, and the speed of the transition will depend on financial possibilities and the political will and decisions, said the panel’s moderator and Director of Zagreb-based Energy Institute Hrvoje Požar Dražen Jakšić.

The acceleration trend in decarbonization is also evident in the electricity market projections for the region until 2030. The plans for the period until the end of the decade include shutting down 6.2 GW of thermal power plant capacity and installing 42.3 GW from renewable sources. Greece, Romania, Serbia and Bulgaria are expected to add the most.

Top executives of state-owned utilities in Serbia, Slovenia and Montenegro and independent power producers that invest in renewables in the region gathered at a panel called Decarbonisation strategies for power generation in Southeast Europe 2040/2050 at Belgrade Energy Forum 2025.

They agreed that decarbonization is well underway and an unstoppable process already speeding up significantly. The participants in the discussion presented the different strategies their companies will act upon in the following years and decades, leading the process to fulfilment.

Among the messages that they shared is that they expect each government to promote investments and make the legal framework clear and certain, while the countries strengthen their ties and exchange experiences. Green energy is the pillar of the energy transition and decarbonization in the region, but several states are also interested in building their first nuclear power plants—conventional ones or small modular reactors (SMRs)—or expanding the existing capacity.

EPS’s Živković: Decarbonization requires energy storage, nuclear plants

Chief Executive Officer of Serbia’s Elektroprivreda Srbije (EPS) Dušan Živković pointed out that the state-controlled electricity producer is committed to its goals regarding green energy and emission reductions as well as to the country’s targets. “We will work on that, of course, believing in these objectives, but without compromising energy security and the energy sovereignty of Serbia. It was proven to be the only sustainable path,” he asserted.

The company particularly counts on the project for solar power plants with a total connection capacity of 1 GW, with batteries of 200 MW in combined capability. The investment is conducted through a strategic partnership with Hyundai Engineering and UGT Renewables (UGTR).

A study is underway in Serbia on the potential for the construction of large nuclear power plants and small modular reactors

The decarbonization process won’t be easily feasible without serious energy storage capacity, Živković warned and added that nuclear energy wouldn’t be unrealistic. A study is underway on the possibilities of building large nuclear plants and small modular reactors in Serbia.

The head of EPS expressed the belief that “the quality of that energy needs to be visualized” for citizens of every country and that they should be explained that it is necessary to provide energy for the economy and its security.

CEOs Dejan Paravan of GEN energija, Dušan Živković of EPS and Eric Scotto of Akuo

No dilemma in Serbia about energy transition

Country Manager of WV-International in Serbia Neda Lazendić highlighted the said strategic partnership for solar power plants with battery energy storage systems (BESS), saying Hyundai Engineering is a world-renowned company.

In her view, the endeavor will be a milestone for the entire region and it is exceptionally important for gaining experience at the domestic level.

The recent second round of auctions for electricity from renewable sources showed that Serbia opted for the energy transition “and there is not any dilemma about it anymore,” Lazendić stressed and said the country is an example for the region. The prices from the bidding that were accepted are appealing and they match European trends, she noted.

Country Manager of WV-International Neda Lazendić

Lignite is highly unprofitable

Slovenia and GEN energija, one of the state-owned power utilities, are relying on both renewable sources and nuclear energy in their decarbonization investments, the company’s CEO Dejan Paravan pointed out.

“We want to get rid of coal as soon as possible. And in the short term, renewables are the only option. Why get rid of coal? The current production of domestic lignite is highly unprofitable, and because of climate goals,” he explained.

Nevertheless, it is exceptionally complicated to get permits for renewables and place them in the environment, Paravan added. On the other hand, nuclear energy is emissions-free and very stable and reliable, he asserted. The technology takes up the least space and enables the production of huge amounts of electricity, the head of GEN energija said.

Nuclear power plant Krško 2 could come online in 2040

Paravan recalled that two years ago nuclear power plant Krško marked four decades since it was commissioned and that its operating life was extended by 20 years. GEN energija is working on the Krško 2 project. The chief executive expects construction to begin in 2022 or 2023 and that the reactor could be connected to the grid in 2040.

In parallel, the company is studying SMRs. Still, the development of the technology will take a long time and, importantly, such facilities won’t have the advantage of scale like large reactors, he said. One who expects electricity from SMRs to be cheaper than from big nuclear plants is wrong, in Paravan’s view.

As for the dilemma between renewable sources and nuclear energy, he expressed the belief that they are not mutually exclusive. “We need renewables and they can provide us a lot of CO2-free electricity in the short run. But let’s make it clear that once we come to 70%, 80%, 90% based on renewables, that we have a problem of seasonal storage, that things will get very difficult,” Paravan stated.

Batteries are ten times cheaper than ten years ago

Conversely, Akuo Energy’s CEO Eric Scotto pointed out that nuclear power is expensive. “It’s over. We won the race. Renewable is the cheapest way to produce energy,” he underscored.

The price of energy storage capacity is ten times lower than ten years ago, the head of the French company noted. Moreover, operating power of a battery system in a standard TEU container, twenty feet or 6.1 meters long, now reaches 6 MW, which is three times more than three years ago, according to Scotto.

To attract investments, stability is necessary, he stressed. Scotto went on to highlight some “simple things” that could help Akuo, which was one of the winners at the last auction round in Serbia, to materialize its projects for two wind parks. He mentioned the speed of permitting for telecommunication systems and road construction, for power plants.

Turning to the slowness of the energy transition in Balkan countries, he emphasized its positive side. “We are late. Then we will benefit from the cheapest resource, the cheapest way to produce energy,” Scotto concluded.

EPCG’s Solari project kicked off energy transition in Montenegro

Technical Director of Elektroprivreda Crne Gore (EPCG) Ljubiša Đurković called the state-owned power utility’s projects Solari 3000+ and Solari 500+ the start of the energy transition in Montenegro. Since the beginning of 2023 and including Solari 5000+, launched later, the company set up photovoltaic systems on 7,380 structures, he revealed.

Total peak capacity reached 76 MW and another 125 MW will be installed by the end of the year, EPCG’s official said.

Among its projects, the company is building the Gvozd wind farm, and the Kapino polje solar park near Nikšić.

Technical Director of EPCG Ljubiša Đurković

There is already 10 MW on roofs in the former Željezara steel plant in Nikšić, and before the end of the year another 15.5 MW will be connected to the grid, Đurković said. A contract has been signed for the construction of the eighth generator in the Perućica hydropower plant, of 58 MW. It is scheduled for completion in 2027.

Đurković: A realistic date for the closure of the Pljevlja thermal power plant is between 2045 and 2050

The energy transition is about a single and connected system, including storage capacities and measures to improve energy efficiency, he underscored. “You have to create the conditions for a swift integration of renewable energy sources into the distribution and transmission networks. We were supposed to do that already. We didn’t do it, particularly in the Western Balkans. We didn’t reconstruct the distribution and transmission networks,” he stated.

As for the current reconstruction of the coal-fired Pljevlja thermal power plant, the only one in Montenegro, Đurković said the project wouldn’t make sense if the facility were to keep operating only for a short while longer.

žAccording to the National Energy and Climate Plan (NECP), which is almost complete, it will remain active at least until 2041, although the realistic date for its closure is only between 2045 and 2050, in the opinion of EPCG’s technical director. The main phase of the reconstruction began at the end of March.

From January 1st, 2026, Carbon Border Adjustment Mechanism (CBAM) will be effective in the Western Balkans. While the countries are still deciding on the carbon pricing model, the energy intensive industry is advocating for introducing taxation to protect the domestic market from the flood of goods that will not be competitive on the EU market. Even though the Governments might not have been proactive enough in the previous years, the participants of the CBAM panel on BEF 2025 believe there is still time for the regional actors to come up with more proactive approach towards the EU.

Energy Community Contracting Parties are approaching critical choices on carbon pricing that will shape the pathway towards climate neutrality, electricity market integration and sustainable economic development. From January 1, 2026, producers of aluminum, fertilizers, cement, steel, and hydrogen, as well as electricity exporters, will be required to pay the tax on CO2 emissions released during the production of the goods they export to the EU.

At the Ministerial Council in December 2024, four carbon pricing models were presented to the Contracting parties: regional emissions trading system (ETS), national carbon taxes, fixed-price Emissions Trading System (ETS), and full integration with the EU ETS. Upon the request of the Contracting parties, the Energy Community Secretariat provided an impact assessment for all four scenarios. The scenarios differ in structure and scope, but all support a common goal: progressive alignment with the EU ETS and the implementation of the polluter-pays principle.

The Ministerial Council is expected to meet in July to reflect on these scenarios and decide on the preferred regional pathway. This decision will shape the revision of the Decarbonisation Roadmap and guide the implementation of carbon pricing reform up to 2030 and beyond.

Carbon pricing is also central to the region’s electricity market future. The Electricity Integration Package, adopted in 2022, outlines the path to full market coupling between the Energy Community and the EU. To avoid distortions and ensure a level playing field, timely carbon pricing implementation is essential. “The projections shows that if the region would join EU ETS after 2030, the carbon price should reach or even exceed 100 euros per ton of CO2. This would have serious consequences for energy prices, competitiveness and industrial exports. Also, delaying actions could prove to be costly. That’s why contracting parties are expecting to implement domestic ETS for electricity with the price equivalent to EU ETS”, Milica Brkić Vukovljak, from Energy Agency of the Republic of Serbia, explained.

Milica Brkic Vukovljak (photo: Balkan Green Energy News)

The expectations around the CBAM introduction in the region were the main topic of discussion on the BEF 2025 panel Addressing carbon pricing in the Western Balkans – Turning decarbonization challenges into opportunities through collaboration, innovation and competitiveness, moderated by Brkić Vukovljak.

The key message from the panel is that regional governments need to take a more active role, especially towards the European Union, and numerous arguments were put forward during the discussion in that direction.

As for Serbia, it is worth noting that it is the only Contracting party of the Energy Community that had transposed the Electricity Integration Package, through which transit of importance for traders takes place. Given that the market coupling is scheduled for the beginning of 2027, it would be important to try to get the European Commission to postpone the deadline from 2026 to 2027.

Introduction of CBAM should not interfere with market integration

While admitting that „it’s never a good moment politically to decide on carbon pricing“, Adam Cwetsch, Head of the European Green Deal in the Energy Community Secretariat, said he believed that the current momentum in the region, together with cumulated experiences, could allow making such a decision at this time.

Adam Cwetsch (photo: Balkan Green Energy News)

He recalled that the decision on carbon pricing was partially left open with the 2021 Decarbonization Roadmap. At the same time, the Green Agenda for Western Balkans is referring to alignment with the EU ETS, as an objective that countries should aim.

„The role of Secretariat is to facilitate making those decisions, fully informed. It entails certain risks, but it is also helping the countries in their journey to join the EU eventually. Another important consideration is setting standards for monitoring emissions, which the countries are obliged to establish and make as of 2026. This is necessary for any credible carbon pricing system, regardless of the chosen model, as they all require credible data and standards“, Cwetsch said.

He insisted that the market integration and market coupling should not be disturbed with the introduction of CBAM, making it a priority to synchronize the situation within the region.

Any model to be decided has to have, as an end point, alignment with the EU ETS

“The least desirable solution would be that there is a country that progresses faster than others and is forced to implement an internal Energy Community CBAM”, Cwetsch said, advocating for a coordinated approach towards setting up the carbon emissions price.

He also noted that any model to be decided must have, as an end point, alignment with the EU ETS. „That should be taken into account when designing the pathway with selected option“, he added.

As things now stand from January 2026 CBAM will be effective, while the market coupling, that allows for exemptions, will not be yet in place. „It is important not to end up with disintegrating the market“, Cwetsch noted.

On the other hand, he believes there is a space for more proactive policy from the Western Balkans actors. „The region should reach out to the EU with more proactive climate policies, which would make clear how the region could contribute to the 2030 or 2040 targets for climate neutrality that EU is striving“, he concluded.

Without carbon pricing mechanisms, the regional markets will be flooded with imports

Branko Zečević (photo: Balkan Green Energy News)

The representatives of energy intensive industry are concerned that past discussions about carbon pricing didn’t pay enough attention to the interests of the companies that are going to be directly affected by imposing tariffs on exports to the EU.

Branko Zečević, president of the Metalfer Group and one of the founders of the Association of Serbian Energy Intensive Industry, said that the introduction of CBAM from the beginning of next year will certainly affect Serbian exports, even though many companies have been preparing for this moment and investing in decarbonization. „Some companies are further down that road, some are at the beginning, and the effects can’t be quantified easily right now“, he argued.

Once you have saved the industry, you have somebody to tax. Otherways, there will be nothing to talk about

However, Zečević insisted that much bigger threat for industry in Serbia and the region, is the expected flood of goods that will not be able to enter EU market anymore and will try to find third markets.

„Markets in the region are pretty opened for that sort of import. An imperative is therefore to have our own carbon pricing system, however you may call it. We must protect our market from these consequences, otherways we will not have any industry to protect in the future“, he insisted.

In his opinion, the first step should be to copy-paste what the EU is doing, to protect the industry, and after that we can talk about the models of carbon pricing. „Once you have saved the industry, you have somebody to tax. Otherways, there will be nothing to talk about“, he warned.

Asked about the expectations of the industry from the Government, he said that financial assistance does not seem a realistic option in the Western Balkans, but there are regulatory measures that could help the companies.

„Industry is more complex than coupling the electricity market, as every industry is different. The companies in the EU received billions of euros in grants over the last 15 years, while the companies in the region were left on their own, each individual company, to make its own adjustments. What the governments in the region can do is to put in place regulatory rules to help and protect local industry and then as a next stage to see if it can implement that regionally“, he concluded.

CBAM ambiguities rising concerns for energy traders

Mark Copley (photo: Balkan Green Energy News)

The ambiguities that follow the introduction of the emissions trading mechanism in the region are more likely to deter than to attract energy traders. Mark Copley, CEO of Energy Traders Europe, association representing 170 energy traders, some of them being active in the region, noted that there is confusion and concern regarding the implementation of CBAM in Western Balkans.

“Lots of questions have been raised: how is that going to work, how the price of CO2 is going to be calculated, what does this means for market integration, how the traders will actually be able to transit power through this region etc”, he said.

Energy traders are pretty good with price risks and volume risks, what we fear is political risk and regulatory risk

While noting that traders generally think that carbon pricing is a good idea, he warned that a good idea in principle could have significant unintended consequences in practice. Energy traders are pretty good with price risks and volume risks, what we fear is political risk and regulatory risk. „I’d like to think that this moment is an opportunity to sit down with all the parties involved to try to sort out the rules”, Copley said.

Copley insisted that he doesn’t have a specific view on what form of pricing is right from the region, but reminded of the experience when Great Britain created its own ETS, which proved to be more volatile, risky and difficult to operate.

„The bigger, more stable, more integrated market – the better. When you have ETS as a large and liquid system, it is fairly easy to trade and manage risks. However, it gets more difficult where you don’t know what the policies are in the short term or in the long term. While I understand the desire that the model should reflect the specifics of the market, be careful in small markets with not much liquidity, because it is hard to design good systems for them”, Copley noted.

Carbon pricing models should reflect the interests of each country in the region

Damir Miljević (photo: Balkan Green Energy News)

The regional non-governmental organizations also have been raising their voice over the topic of CBAM in previous years. One of the warnings of possible negative economic and social impacts was the analysis Chaotic and fake decarbonization of power sectors in the Western Balkansin 2023.

“The problem is that the introduction of CBAM in often seen as a kind of natural disaster, something inevitable that is about to happen”, said Damir Miljević, member of the Board of Center for Sustainable Energy Transition, RESET, a think-tank that published the report mentioned.

In his opinion, Western Balkan countries did not participate actively in the process with lobbying and negotiating with the EU. „The policy makers sit in Brussels, while the Energy Community Secretariat is the directorate for the implementation of the international agreement. I don’t recall that some delegation from the Western Balkans went to talk to the EU about exemptions, even though we had at least one strong argument. Stabilization and Association Agreement with the EU states that neither contracting party will introduce additional taxes, or levies on the other, which means that even if they are introduced, we would have to negotiate about it“, Miljević explained.

The advantage should be given to the model that is fastest and simplest to implement, which is direct taxation

Another argument for negotiations is even stronger – the countries that are candidates for EU accession should not have the same treatment as some very distant states on other continents, he argued. Miljević also added that the region should focus on transferring the acquis from the EU, which they are obliged to, not the policies, where the situation is completely different.

„In the present situation, the only viable solution is to introduce some form of taxation of CO2 for the industry“, he said. In his opinion, this means the advantage should be given to the model that is fastest and simplest to implement, which is direct taxation, to eliminate the influence of CBAM on the export of industrial products from the region to the EU.

„It would be difficult to consider regional schemes, due to huge differences within the region. We already lost too much time on it. Each country should do it individually considering its own interest, not the interest of the energy sector, but the interest of the citizens and the economy and the consequences for them. This way, we will get some initial, however small assets, to start solving the core issue. We should also remember that the introduction of levies on CO2 is essential for the creation of any fund for coal regions in transition”, Miljević concluded.

The deployment of battery energy storage systems (BESS) across Southeast Europe is progressing at an uneven pace. State subsidies and financing mechanisms have enabled the rapid implementation of BESS solutions in Greece, Romania and Bulgaria, while markets in the Western Balkans are lagging behind. However, the outlook remains positive, as experiences from neighboring markets and best practices from other parts of the European Union can help overcome initial challenges and streamline the deployment process. This was highlighted by participants of the panel dedicated to BESS at the Belgrade Energy Forum.

Among the technologies required for the energy transition, battery energy storage systems (BESS) stand out as a key factor for integrating electricity from intermittent renewable sources – wind and solar power – into the grid. There are few such facilities in Southeastern Europe and the segment is yet to even be fully regulated in the narrower Western Balkans region. The panelists at a session called Energy storage system market in SEE: trends and forecasts, at Belgrade Energy Forum (BEF 2025), outlined the trends in the budding market.

There are more and more cases of low and negative hourly prices in the wholesale electricity market in the region, providing a clear business case for BESS investments. In addition, the grid is often overloaded on weekends and holidays when solar and wind power production is high, given the weak demand.

Managing Director of Go2Power Consulting Goran Vukojević, who moderated the discussion, warned that negative prices may jeopardize system stability as well, if operators of power plants disconnect them from the grid at the same time, to avoid costs.

He highlighted the preparations in Serbia’s transmission system operator Elektromreža Srbije (EMS) for auctions for ancillary services and praised the company for transparency in regulating the competitive process. The other option for battery operators is to participate in the open market.

Managing Director of Go2Power Consulting Goran Vukojević moderated the panel discussion

Region seen with 9 GW of BESS operating power in 2030

Ioanna Barouni from Aurora Energy Research said a total of 40 GW of solar and wind power is expected to be online at the end of 2025 in the SEE region, comprising 12 countries, including Hungary. In 2030, the level is expected to reach 70 GW, which is expected to be doubled to 145 GW by mid-century. As for BESS, projections stand at 9 GW in 2030 and 25 GW in 2050.

Barouni: We miss flexibility and ancillary services for transmission and distribution system operators

The countries of the region are retiring power plants that use fossil fuels, a firm capacity, in Barouni’s words, while adding renewables. “It’s not very easy to predict how the generation profile is going to be during the day, so we miss flexibility and we miss ancillary services for TSOs and DSOs,” she said.

The gap between power prices for midday and the evening is gradually increasing. Barouni explained that batteries “create some artificial demand and absorb these low prices.” At peak demand and with less renewables, a battery can replace expensive fossil fuels, lowering the price.

Ioanna Barouni from Aurora Energy Research (pictured left) and Head of Specialized Lending at UniCredit Bank Serbia Svetlana Cerović

Serbia preparing auctions for ancillary services

Division Manager of transmission system operator (TSO) EMS Nikola Tošić acknowledged that Serbia is preparing auctions for ancillary services. He revealed that there would probably be one auction for 70% of the needed reserve in the first year. The next rounds would be more frequent, shifting toward daily auctions for balancing capacity.

In the verification process, EMS’s System Operation Department will first test the battery, Tošić added. State-owned power utility Elektroprivreda Srbije (EPS) already provides ancillary services to the TSO, so it won’t require tests, he asserted.

Serbian law defines ancillary services the same as European Union does

EMS drafted the new grid code, and it will publish the draft balancing market code for public discussion soon, according to Tošić. He said the domestic law defines ancillary services in the same way as the EU defines them in its legislation. One part is balancing services: frequency containment reserve (FCR, primary), automatic frequency restoration reserve (aFRR, secondary) and manual frequency restoration reserve (mFRR, tertiary). The other part are non-frequency services – energy.

“We think that it would be good to incentivize the periods of the year or periods of day when the needed amount of reserve is more attractive or more in demand,” Tošić said.

Market Division Manager of EMS Nikola Tošić

Fortis Energy moving ahead with battery investments regardless of government support schemes

Fortis Energy’s Chief Executive Officer for Eastern Europe Nikola Oklobdžija considers the lack of regulation to be the biggest challenge for developers. An investor can currently only focus on charging the batteries when the prices are low and sell when they are high, he underscored.

The Turkey-based company develops photovoltaic, wind power and BESS projects in the region. The first bigger investments in renewable electricity plants with energy storage are the ones that will break the ice, in Oklobdžija’s opinion.

“Of course, it helps if you have a CfD contract, so the banks will look at it more favorably,” he stated. Oklobdžija added that companies need to be able to present revenue to the lenders and what the fees are for renting the capacity or providing different services.

Bankability depends on state support and PPA contracts, cash flow models and insurance

In the meantime, Fortis is examining the experiences in Bulgaria and Greece, which have already held auctions for standalone batteries. Financing a project is easier with a CfD – contract for difference, but the company is determined to push ahead anyway, Oklobdžija stressed.

In North Macedonia it commissioned a solar power plant in Oslomej and recently contracted a BESS to be added to the facility. Oklobdžija said it wasn’t a requirement but that Fortis opted for energy storage because of market pressure with prices and occasional curtailments, like during Easter last month.

The introduction of ancillary services would facilitate the development for standalone battery systems, he explained.

Fortis Energy’s CEO for Eastern Europe Nikola Oklobdžija

Cerović: First there will be more projects for colocated BESS units than for standalone facilities

Head of Specialized Lending at UniCredit Bank Serbia Svetlana Cerović highlighted the intensive activity in Germany and Italy, for instance, but also in neighboring Romania. UniCredit is present in those markets and is analyzing the development of the battery storage market, she pointed out, arguing that the best practices in the EU are the best way for building and financing battery storage.

Cerović said there would first be more projects in the region for BESS colocated with renewable energy plants than standalone units.

She suggested that the proposed investments that include storage should be better pondered at the next renewable energy auction in Serbia. It is in the country’s interest to enable providing flexibility and to support the projects, she said.

There may be a rationale for subsidizing prosumers to add storage in Serbia, Cerović said. Turning to small-scale projects, she expressed the belief that power purchase agreements (PPAs) are “convenient” for them. She is recommending dedicating a certain capacity for the category at the next auction in the country.

The first projects in Serbia, conditioned by energy storage requirements for a grid connection, are in the process of negotiating financing, according to Cerović.

Fire protection is especially significant for insurers

Renewable Energy Insurance Broker (REIB) has insured some 4 GWh of energy storage capacity in Bulgaria and just as much elsewhere in the world, Business Development Manager Dimitar Dimitrov said. Developers should contact insurance companies when the design is done, as well as for cargo insurance, he suggested and added it is particularly important for projects that get subsidies.

“We’re not only insurance brokers, but we’re also investors, which helps us understand a bit more about the clients’ needs, and what we can definitely do more in cases of coverage. Understanding clients’ needs helps us also prevent risks that could occur during certain stages,” Dimitrov stated.

Most insurers prefer at least a six-meter distance between containers or rows of three to four containers holding batteries, he said. It is the most important factor in fire protection, in Dimitrov’s opinion. When the distance is shorter than three meters, a firewall is required for insurance, he explained.

REIB’s Business Development Manager Dimitar Dimitrov

The next segment is construction insurance. For insurance companies, it is not a higher risk profile, Dimitrov asserted. Next, he recommended operational risk insurance including coverage for business disruption, and insurance against cyberattacks. In such events, the grid connection can be damaged, the company’s representative pointed out. “Insurance policies are definitely bankable,” he added.

Bulgaria has completed its tenders for state support to BESS combined with renewable energy plants, and for standalone units. But even before subsidies, batteries have been delivered and facilities are under construction, Dimitrov stressed. Many photovoltaic projects in Bulgaria have emerged in the past few months and most of them include BESS, he said.

Capacity building and education for corporates, together with product diversification and an upgrade of the regulatory framework, could clear the obstacles for power purchase agreements in the Western Balkans, which are lagging behind the other countries in Southeast Europe. In addition to their other benefits, such contracts could contribute to securing baseload energy from hybrid facilities, given that baseload is a key issue for the decarbonization of the region, according to the participants of a panel on power purchase agreements, held at Belgrade Energy Forum 2025 (BEF 2025).

BEF 2025 has gathered four hundred participants from more than 30 countries in the region, Europe, and beyond.

The panel PPAs as a key to renewable energy growth in SEE featured stakeholders from all segments of the PPA market: developers, corporates, utilities and consultants. The discussion comprised five segments – the global trends, main drivers, the region’s specifics, challenges and trends, and the implications of the model.

The panel’s moderator was Mislav Slade-Šilović, Energy, Utilities & Resources Consulting Leader for Southeast Europe and member of the core PPA team at the consultancy PwC.

Global trends: PPAs are hot, but the solar capture rate is becoming an issue

Mislav Slade-Šilović, Joffroy Beckers and Nikola Gazdov

According to Natalija Ljubić, Manager of PPA & BESS Transactions at Pexapark, PPAs are still hot in Europe. On a monthly basis, between 500 MW and 2,000 MW of new PPAs are signed (15 to 30 deals). She referred to long-term, fixed-price PPAs considered bankable and publicly announced. There is much more together with short-term PPAs, for two to three years.

There is an impression that everything comes down to corporate PPAs, but there are many utility PPAs that aren’t always made public, she added.

The majority are physical PPAs but Pexapark is registering more and more financial PPAs. In 2025, almost 20% of all the announced PPAs were financial, whereas a couple of years ago, they made up 5% to 10%. There are more pay-as-produced contracts than the monthly ones for baseload energy.

Mislav Slade-Šilović (PwC) added that 70% of PPAs in SEE are virtual or financial.

It’s quite challenging in the region to find a creditworthy counterparty on the consumer side

For developer Joffroy Beckers, Head of PPA at DRI, it’s quite challenging to find a creditworthy counterparty on the consumer side of the market in the region comprising Greece, Bulgaria and Romania. So when the firm wants to speed things up with selling its electricity, it goes to utilities or traders.

Negative prices are emerging in the region, with much more cannibalization for solar in the long term, he added.

According to Bulgaria’s Association for Production, Storage, and Trading of Electricity – APSTE, the situation in the region is different than five years ago. “There were zero PPAs in the region, but now they start to get common. Paradoxically, the conditions start getting much more and more complex,” chairman Nikola Gazdov said.

Mislav Slade-Šilović (PwC) pointed to the decline in the solar capture rate – the ratio of the price of solar power and wholesale price. It is spilling over to the PPA price and increasing its complexity, and solar PPAs are generally more complex than the ones for wind power, he added.

Main drivers: Different priorities ask for different PPA models

Natalija Ljubić, Ivana Đurović and Davor Pupovac

For Ivana Đurović, Category Manager Renewable Energy at Knauf Group, PPAs are a game changer in energy procurement because essentially it’s no longer just about buying energy or hedging. “Now corporate PPAs bring the long-term deal, so they even extend the tenure for those hedging, and they also allow us to achieve our sustainability targets,” she explained.

PPAs aren’t for companies with consumption below 30 GWh or 40 GWh per year, while branding and cost savings are often the reasons for companies to sign them.

Such factors determine the PPA product that the offtaker opts for, Mislav Slade-Šilović (PwC) stressed.

According to Nikola Gazdov (APSTE), in the region comprising Bulgaria, Romania, and Greece, PPAs are usually signed by corporates that have some ESG commitments or want to show their clients and customers that they are thinking green.

The key feature of a PPA is the partnership between two companies

As examples of the various kinds of deals, he mentioned a physical PPA with an electricity-intensive consumer, virtual PPA with a telecom and a PPA with a big international company producing tires, combining the two types.

As a developer, DRI is modifying its strategy toward a mixed portfolio. Instead offering a solar asset for a PPA, it adds wind power plants and combines different technologies into a single contract. “It allows us to capture a better price, and this is also usually more beneficial for the off-taker. The second thing is that we’re trying to keep this upside in our PPA by entering a floor price instead of a fixed price,” Joffroy Beckers (DRI) revealed.

For Mislav Slade-Šilović (PwC) the key characteristic of a PPA is the partnership between two companies. It needs to be balanced, to ensure that both parties can fulfill throughout the tenure. If one goes bankrupt, then it doesn’t make sense for both parties, he underlined.

The specifics in the region: Corporates need to learn, PPAs should be more diverse

Nikola Gazdov, Natalija Ljubić and Ivana Đurović

Serbia’s state-owned power utility Elektroprivreda Srbije (EPS) has been signing a lot of PPAs. However, the difference from the conventional deals is that they are based on premiums. But according to Davor Pupovac, head of the company’s market analysis and risk management, it is interested in corporate PPAs that don’t include government support. There is not much interest among consumers for corporate PPAs with EPS, he revealed.

Mislav Slade-Šilović (PwC) said the role of EPS and big power utilities is very important in developing the PPA market. A dominant supplier in a market has a critical role, either as a sleever or as someone that will provide B2B products to off-takers and developers or producers for entering the market, he said.

Joffroy Beckers (DRI) agreed with him about the role of big utilities in facilitating PPAs and expressed the belief that in the near future, they would get a larger share as intermediaries.

Asked if corporate PPAs are coming anytime soon in Serbia, Davor Pupovac (EPS) said: “Not so soon.” However, he claimed EPS wouldn’t lose consumers regardless of the fact that it has no such product.

Corporates aren’t super ready for PPAs because they are seeking stability when it comes to the energy price

In Ivana Đurović’s (Knauf) view, there are several reasons for the slow uptake of corporate PPAs in the Western Balkans. Corporate buyers aren’t super ready for PPAs because they are seeking stability when it comes to the energy price, but the pay-as-produced PPA model is dominant in the market, which doesn’t ensure price stability. Monthly baseload deals would enable more price stability.

A bigger offtake through PPAs requires corporates to build their capacity for closing such deals and for the offer to be more diverse, she stressed.

Natalija Ljubić (Pexapark) agreed with her and suggested that companies need to understand more about the risks and accounting. Also, not many corporates are willing to enter five- to ten-year agreements as they don’t know their demand or costs that far ahead, Ljubić underlined.

Challenges, risks: Management boards are delving into energy-related topics in detail

Ivana Đurović and Davor Pupovac

Creditworthiness is one of the key challenges, Joffroy Beckers (DRI) said. As he sees it, credit insurance could be key, providing a kind of a state guarantee. Nikola Gazdov (APSTE) again stressed education. He also recalled that all European countries needed time to get along with PPAs.

“But coming to credit risk, I think that now we also see the European Commission taking note of the situation,” Gazdov noted.

As for education, Mislav Slade-Šilović (PwC) said it requires one to two years. Management boards of companies from different industries on the offtake side are forced to delve into energy-related topics in detail, he noted.

There are practically no obstacles for PPAs in Serbia

Slade-Šilović asked EPS’s representative whether the utility is prepared to offer B2B products, arguing that they go hand-in-hand with PPA market development.

Davor Pupovac (EPS) responded that there are practically no obstacles to PPAs in Serbia. Namely, there is an electricity exchange, EPS is willing to sign contracts with developers for sleeving or balancing, the guarantees of origin (GO) system is in place, and EPS is active on power exchanges in the region as a producer and supplier.

“EPS could also offer a route to market to the off-taker. However, currently, it cannot offer access to the spot or forward market,” he explained.

Coming from a corporate electricity consumer, Ivana Đurović (Knauf) was curious what EPS could offer to a perfect corporate off-taker asking for a physical PPA. Pupovac answered that currently it would be a pay-as-produced deal.

What does the implementation bring us: hybrid combinations open the room for innovative deals

Joffroy Beckers, Nikola Gazdov and Natalija Ljubić

Mislav-Slade Šilović (PwC) summarized the landscape. “If you look at the broader EU situation and challenges, especially with solar capture rates, negative prices, we are now already discussing technology advanced structures including batteries and other hybrid solutions on the PPA side,” he underlined.

Natalija Ljubić (Pexapark) pointed out that last month in Germany the solar capture rate was just 40%, calling it almost unbearable for photovoltaic projects. All developers or energy producers, especially in the solar power sphere, are seriously considering adding batteries, while projects for standalone battery storage facilities are appearing, in her words.

She and Nikola Gazdov (APSTE) agreed that the outcome is a lot of interesting innovative structures, room for different solutions.

BESS with solar reduces cannibalization and increases capture rates

Ljubić said it is a challenge to maximize revenues from a battery system and make it bankable. Gazdov pointed to the dilemmas of a single company owning different assets versus a big utility combining and aggregating everything, and whether the producers or optimizers manage the revenue streams.

When it comes to standalone storage units, he sees a perspective only in arbitrage and, perhaps, system services further down the road.

Joffroy Beckers (DRI) explained the main purpose of a battery energy storage system (BESS) in Romania, from the point of view of a developer and power producer. A BESS combined with solar power reduces cannibalization and increases capture rate, whereas wind lowers the balancing cost, he stressed.

“If you co-locate a battery next to solar, you will be in a position to negotiate a higher price on the off-take side,” he pointed out.

A combination of wind, solar and batteries is equivalent to a new power plant

In the future, he anticipates more PPAs with a pay-as-nominated structure rather than pay as produced, arguing that it enables more flexibility for monetizing batteries on different markets.

“With those combinations of wind, solar, and battery, basically you have a new power plant, baseload structure,” Mislav Slade-Šilović (PwC) stated.

That way PPAs fit into the broader discussion on the energy transition and decarbonization. EPS is decarbonizing its production through its role as a renewable energy offtaker.

“Hybrid combinations are partly addressing the baseload needs. So, many different technologies, including storage, can provide a part of the answer this region heavily needs, and this is the baseload substitution problem,” Slade-Šilović concluded.